📑 Table of Contents

- 1. Make Prepayments Whenever Possible

- 2. Opt for a Shorter Loan Tenure

- 3. Increase EMI with Your Income Growth

- 4. Transfer Your Home Loan to a Lower Interest Rate

- 5. Use Windfalls Wisely

- ✅ Conclusion

- 🧾 Quick Recap Table

- ❓ Frequently Asked Questions (FAQs)

Buying your own home is one of the biggest milestones in life. However, a home loan often comes with a long repayment tenure and high interest costs. The good news? With a few smart financial decisions, you can repay your home loan faster, save a large chunk of money, and enjoy complete peace of mind.

Let’s explore five proven ways to close your home loan early while maintaining financial stability.

🏦 1. Make Prepayments Whenever Possible

Making lump-sum prepayments is one of the simplest and most effective strategies to reduce your home loan burden. Whenever you receive extra income — like annual bonuses, tax refunds, or matured investments — use a portion of it to pay down your principal.

Example:

If you have a ₹40 lakh home loan at 8.5% for 20 years and prepay ₹1 lakh every year, you can save over ₹7 lakh in interest and close your loan 3–4 years earlier.

Tip: Floating-rate home loans usually have no prepayment penalty, so take full advantage of this flexibility.

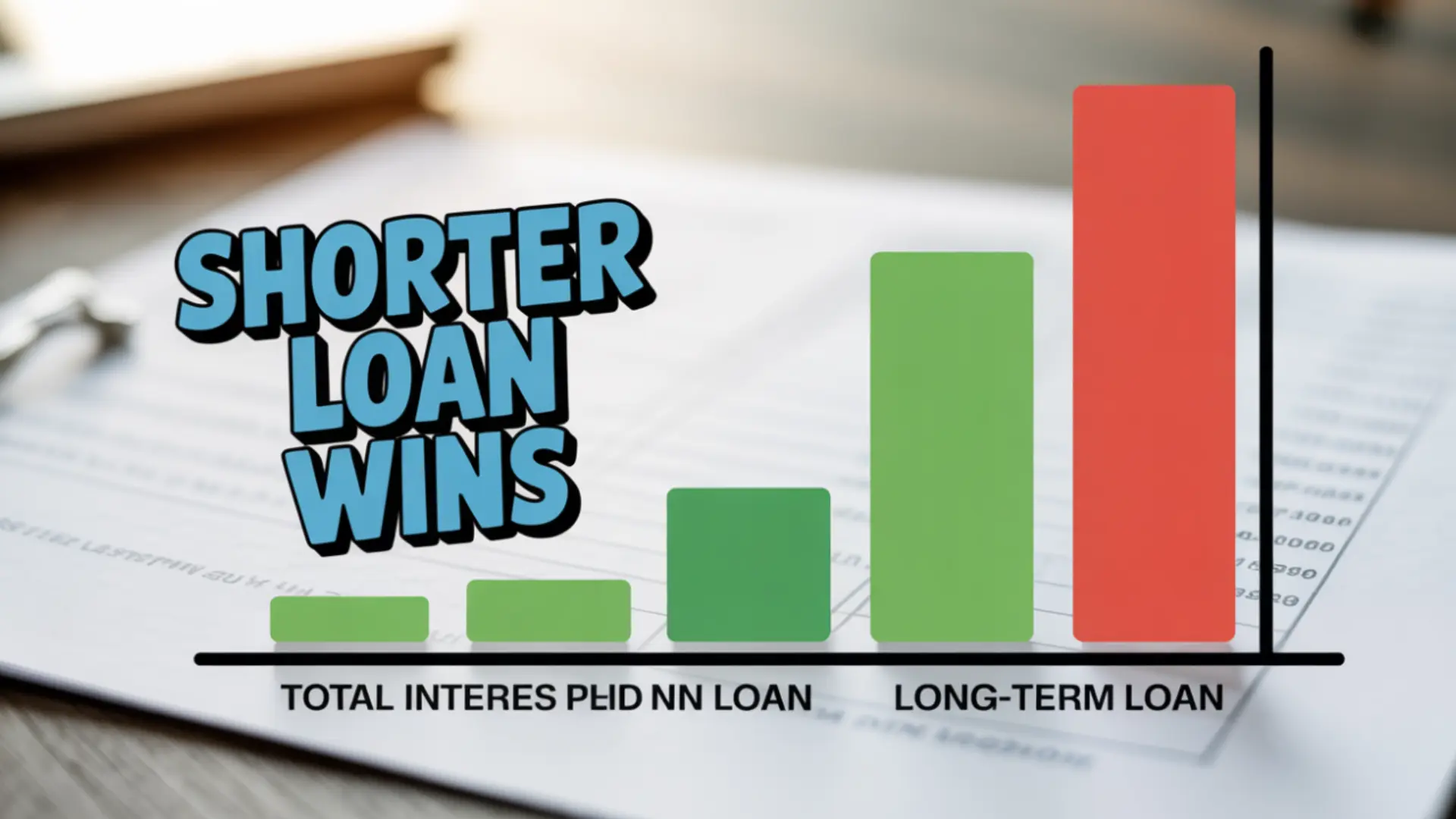

⌛ 2. Opt for a Shorter Loan Tenure

A shorter tenure means slightly higher EMIs but much lower interest costs in the long run. While a longer tenure feels comfortable, it results in a much higher total repayment amount. If your income allows, always opt for a shorter loan period.

Example:

- ₹40 lakh loan at 8.5% interest:

- 20 years: EMI ₹34,785; Total Interest ₹43.4 lakh

- 15 years: EMI ₹39,403; Total Interest ₹30.9 lakh

Saving: ₹12.5 lakh simply by choosing a shorter tenure!

💹 3. Increase EMI with Your Income Growth

Your income usually increases over time — through promotions, raises, or business growth. Instead of spending the extra amount, consider increasing your EMI. Even a 5–10% annual increase in EMI can reduce your loan tenure drastically.

Example:

If you start with an EMI of ₹35,000 and increase it by 10% every year, you could repay a 20-year loan in just 12–13 years — saving lakhs in interest.

🏦 4. Transfer Your Home Loan to a Lower Interest Rate

Interest rates vary across lenders. If your current lender is charging a higher rate, you can refinance or transfer your home loan to another bank offering a better deal. Even a small reduction in rate (0.5%–1%) can save you lakhs of rupees.

Example:

For a ₹40 lakh loan with 15 years left, reducing the rate from 9% to 8% can save over ₹3 lakh in interest.

Tip: Compare processing fees and hidden charges before switching to ensure net savings.

💰 5. Use Windfalls Wisely

Whenever you receive unexpected income — such as a bonus, inheritance, or matured investment — consider using part of it to make a one-time prepayment. This simple step reduces your outstanding principal and loan tenure.

Example:

If you use ₹5 lakh from a matured FD to prepay your home loan, you could close it 2 years early and save a huge amount on interest.

✅ Conclusion

Paying off your home loan faster gives you more than just savings — it gives you financial freedom and peace of mind.

By following these five strategies:

- Make prepayments regularly

- Choose a shorter tenure

- Increase EMI gradually

- Transfer to a lower rate

- Use windfalls wisely

You can become debt-free years ahead of time and redirect your money toward investments and future goals. Remember, the earlier you start, the greater the savings!

🧾 Quick Recap Table

| Strategy | Key Benefit |

|---|---|

| Make Prepayments | Reduces principal and interest burden |

| Choose Shorter Tenure | Saves lakhs in total interest |

| Increase EMI | Speeds up repayment without financial stress |

| Transfer to Lower Rate | Lowers EMI and total interest |

| Use Windfalls | Cuts down loan balance instantly |

❓ Frequently Asked Questions (FAQs)

1. Is it good to repay a home loan early?

Yes, repaying your home loan early reduces your overall interest cost and gives you financial peace. However, ensure that you still maintain enough savings for emergencies before prepaying aggressively.

2. Does prepayment reduce EMI or tenure?

You can choose either option:

- Reduce EMI – to ease your monthly burden.

- Reduce tenure – to close the loan faster and save on interest.

Reducing tenure usually offers more long-term savings.

3. How often can I make prepayments?

Most banks allow multiple prepayments in a year on floating-rate loans without penalties. Check your lender’s policy for fixed-rate loans.

4. Should I use all my savings to repay the home loan?

No. Always keep an emergency fund (6–12 months of expenses) before using savings for prepayment. Balance your debt repayment with liquidity needs.

5. Is transferring my home loan to another bank worth it?

Yes, if your new lender offers at least 0.5–1% lower interest rate and the transfer costs are reasonable, refinancing can be highly beneficial.

Final Tip: Be disciplined, review your loan regularly, and make smart repayment decisions. A faster home loan closure isn’t just about saving money — it’s about achieving complete financial independence. 🏡💡

{kind=link}